Here is the full text of my article for the Economic Times-Corporate Dossier (issued dated October 19, 2007)

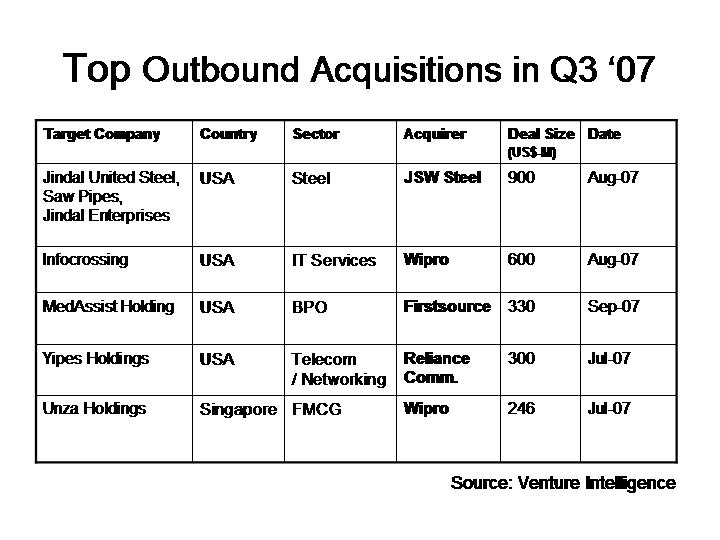

Despite the liquidity crunch in the US and Europe, Indian companies are stepping on the accelerator when it comes to acquiring overseas companies. Indian companies have closed over 60 outbound acquisitions worth over $4 billion during the latest quarter – i.e., amidst the “sub-prime crisis”. These included 15 deals that cost over $50 million and six that with tags of over $200 million!

Click Here for a table on top outbound acquisitions during the latest quarter.

So, why the hurry? One answer is the opportunity presented by the near absence of competition from LBO (Leveraged Buyout) firms. With lenders turning off the taps for cheap debt, LBO firms are no longer able to outbid strategic buyers with ease. This could be prompting the strategy and M&A heads at Indian companies to think what’s a few basis points here and there when the lack of alternative buyers can shave off a few millions on the target’s price? Plus, an ever rising rupee is only making overseas assets that much cheaper to acquire. We are hoping to get more insights on what makes cross-border acquisitions tick from a host of experts – including from companies like Suzlon Energy, Spentex Industries, Geometric Software, Take Solutions, UTI Ventures and others - at the Venture Intelligence M&A Summit in Mumbai on October 25.

New Sources of Liquidity

Private Equity firms exited their investments in 34 companies during the first six months of 2007 via M&A deals compared to just 26 such exits during the entire of 2006. The rising number of M&A exits is driven by two trends. The first - and slightly older trend – is that of MNCs acquiring companies in India to “hit the ground running” in terms of market access and capabilities. While this has been driving acquisitions the IT & ITES industry (think IBM-Daksh, EDS-Mphasis, etc.), what’s new this year is the acquisition by MNCs in consumer targeting businesses – good examples being Hershey’s acquisition of Godrej Foods and Norway-based Orkla Foods’ acquisition of MTR Foods.

The other – newer – trend is the rising acquisitions of PE-backed companies by other PE firms. The number of such deals, known in PE industry parlance as “secondary sales”, is growing thanks to the ever increasing number of new PE firms entering the market. And it is giving existing funds a nice source of liquidity for their investments. Last year, we had witnessed several such deals in IT & ITES companies including SAIF’s buyout of Baring India from CSS Group and Carlyle providing liquidity to Euronet Ventures from Allsec Technologies. This year the trend has again moved beyond IT exemplified by the acquisition of APIDC VC’s stake in Hyderabad-based port management firm Ocean Sparkle by India Equity Partners.

It is not just strategic acquirers and new PE entrants that are providing liquidity to existing PE & VC firms. A new category of investors - Special Purpose Acquisition Corporations or SPACs – are promising to open up another avenue on the exits front. (SPACs, also called “blank check” companies - are newly-formed companies without assets, whose sole purpose is to acquire an unidentified company in a targeted industry.)

Several India-focused SPACs have raised (or filed to raise) capital via IPOs on the US and European exchanges and are scouring the country for acquisition opportunities. They include the Phoenix India Acquisition Corp., Global Services Partners Acquisition Corp. and TransTech Partners (all of which are IT focused); Trans-India Acquisition Corp. (which is focused on Life Sciences) and Millennium India Acquisition Company (which has a broader focus including financial services, healthcare, infrastructure, retail and hospitality).

Malaysia-based PE firm Navis Capital, which had developed a strong taste for Indian food and restaurant businesses, has found an exit route for its investments in three such companies – Mars Restaurant, SkyGourmet Catering and Nirula’s – via a sale to India Hospitality Corp, a SPAC listed on the London AIM exchange.

Tail piece

Build to flip or build to last? Using an interesting analogy, K. Ganesh, Founder & CEO of TutorVista and a serial entrepreneur who has successfully exited three ventures, provided an answer to this eternal start-up question while speaking at a recent Venture Intelligence conference. Ganesh compared building a company to that of building a house.

Depending on whether you plan to sell the house or rent it out or live in it, you would build and furnish the property differently. Similarly, depending on their vision for their businesses, the approach of entrepreneurs who planned to exit the business after building value over a few years would vary from that of others who intend to pass it on to their children. However – whether a company is built to last or flip - in order to create a significantly valuable business, it is critical for an entrepreneur to be passionate about the core idea and willing to “bet his or her life on it”.

Arun Natarajan is the Founder & CEO of Venture Intelligence, the leading provider of information and networking services to the private equity and venture capital ecosystem in India. View free samples of Venture Intelligence newsletters and reports.

Despite the liquidity crunch in the US and Europe, Indian companies are stepping on the accelerator when it comes to acquiring overseas companies. Indian companies have closed over 60 outbound acquisitions worth over $4 billion during the latest quarter – i.e., amidst the “sub-prime crisis”. These included 15 deals that cost over $50 million and six that with tags of over $200 million!

Click Here for a table on top outbound acquisitions during the latest quarter.

{kind=link}

So, why the hurry? One answer is the opportunity presented by the near absence of competition from LBO (Leveraged Buyout) firms. With lenders turning off the taps for cheap debt, LBO firms are no longer able to outbid strategic buyers with ease. This could be prompting the strategy and M&A heads at Indian companies to think what’s a few basis points here and there when the lack of alternative buyers can shave off a few millions on the target’s price? Plus, an ever rising rupee is only making overseas assets that much cheaper to acquire. We are hoping to get more insights on what makes cross-border acquisitions tick from a host of experts – including from companies like Suzlon Energy, Spentex Industries, Geometric Software, Take Solutions, UTI Ventures and others - at the Venture Intelligence M&A Summit in Mumbai on October 25.

New Sources of Liquidity

Private Equity firms exited their investments in 34 companies during the first six months of 2007 via M&A deals compared to just 26 such exits during the entire of 2006. The rising number of M&A exits is driven by two trends. The first - and slightly older trend – is that of MNCs acquiring companies in India to “hit the ground running” in terms of market access and capabilities. While this has been driving acquisitions the IT & ITES industry (think IBM-Daksh, EDS-Mphasis, etc.), what’s new this year is the acquisition by MNCs in consumer targeting businesses – good examples being Hershey’s acquisition of Godrej Foods and Norway-based Orkla Foods’ acquisition of MTR Foods.

The other – newer – trend is the rising acquisitions of PE-backed companies by other PE firms. The number of such deals, known in PE industry parlance as “secondary sales”, is growing thanks to the ever increasing number of new PE firms entering the market. And it is giving existing funds a nice source of liquidity for their investments. Last year, we had witnessed several such deals in IT & ITES companies including SAIF’s buyout of Baring India from CSS Group and Carlyle providing liquidity to Euronet Ventures from Allsec Technologies. This year the trend has again moved beyond IT exemplified by the acquisition of APIDC VC’s stake in Hyderabad-based port management firm Ocean Sparkle by India Equity Partners.

It is not just strategic acquirers and new PE entrants that are providing liquidity to existing PE & VC firms. A new category of investors - Special Purpose Acquisition Corporations or SPACs – are promising to open up another avenue on the exits front. (SPACs, also called “blank check” companies - are newly-formed companies without assets, whose sole purpose is to acquire an unidentified company in a targeted industry.)

Several India-focused SPACs have raised (or filed to raise) capital via IPOs on the US and European exchanges and are scouring the country for acquisition opportunities. They include the Phoenix India Acquisition Corp., Global Services Partners Acquisition Corp. and TransTech Partners (all of which are IT focused); Trans-India Acquisition Corp. (which is focused on Life Sciences) and Millennium India Acquisition Company (which has a broader focus including financial services, healthcare, infrastructure, retail and hospitality).

Malaysia-based PE firm Navis Capital, which had developed a strong taste for Indian food and restaurant businesses, has found an exit route for its investments in three such companies – Mars Restaurant, SkyGourmet Catering and Nirula’s – via a sale to India Hospitality Corp, a SPAC listed on the London AIM exchange.

Tail piece

Build to flip or build to last? Using an interesting analogy, K. Ganesh, Founder & CEO of TutorVista and a serial entrepreneur who has successfully exited three ventures, provided an answer to this eternal start-up question while speaking at a recent Venture Intelligence conference. Ganesh compared building a company to that of building a house.

Depending on whether you plan to sell the house or rent it out or live in it, you would build and furnish the property differently. Similarly, depending on their vision for their businesses, the approach of entrepreneurs who planned to exit the business after building value over a few years would vary from that of others who intend to pass it on to their children. However – whether a company is built to last or flip - in order to create a significantly valuable business, it is critical for an entrepreneur to be passionate about the core idea and willing to “bet his or her life on it”.

Arun Natarajan is the Founder & CEO of Venture Intelligence, the leading provider of information and networking services to the private equity and venture capital ecosystem in India. View free samples of Venture Intelligence newsletters and reports.